The number of banks in Germany has been in continuous decline over the past few decades, reflecting pressure to rationalize and cut costs. Despite this shrinking of the market in terms of institutions number, the size of the German banking system in terms of total assets to GDP (Gross Domestic Product) increased steadily until the subprime financial crisis.

Following the financial crisis, large German banks, particularly Landesbanken, have scaled back their interbank activities and foreign operations. ¹ The cost of financial intermediation seems to have declined due to improved technology and increased competition. ²

How digital innovations affect productivity in banking crucially depends on changes in the competitive structure of markets. As in other industries, the entry of new, more productive firms and the exit of incumbents can be a channel for productivity improvements. ³

Nowadays, neobanks are under tremendous pressure to show they mean business. Investors are pushing the fintech challengers to demonstrate that they are able to monetize their products and eventually make a profit. And those conditions are perfect for some kind of market consolidation.

The challengers have been racing to roll out new products in an effort to bring in new revenue streams and edge toward profitability. They are typically confronted with increasing costs, while the margins generated per customer remain low. Although several years of losses and heavy venture capital investing are standard requirements to disrupt the financial market, some indicators, such as the LTV/CAC ratio, should still be healthy.

The LTV (the customer Life-Time Value) is the average revenue generated by a customer in 1, 3 or 5 year period. This should be as high as possible but remains an area of concern for many neobanks that seek revenue mainly from the low debit card interchange fees. The average LTV is around EUR 15 per customer per year and can worsen due to reduced traveling and small purchases following different confinement periods.

The CAC (Customer Acquisition Cost per customer) is the total money spent on customer acquisition divided by new customers. This should be as low as possible. Most neobanks still achieve far better CAC values than incumbent banks, with an average CAC of neobanks around EUR 30 versus EUR 200 for incumbent banks, but still too high compared to the average revenue generated per customer.

As a result and enforced by the recent pandemic and its effects on the economy, venture capital firms start to push neobanks to change their focus from growth to profitability. This condition leads to neobanks repositioning their offering, seeking more profitable products and services, like investments and credits. Other strategies to increase LTV are expanding to more profitable customer segments, like SMEs, providing “banking-as-a-service” to other fintechs or even banks, and positioning their fintech app as a super-app offering third-party non-financial services and taking a lead generation commission. ⁴

Several well-funded fintech companies that exclusively focus on serving the freelance or SME market segment have been founded in Europe over the last years. ⁵ However, the profitability urgency has positively impacted the early-stage entrepreneurial ecosystem, once freelancers, startups and SMEs have been the center of many neobanks strategies. Products and services targeted in this public have supported the initial company phase that, in general, has more severe difficulties to stay alive in the market.

More than ever, businesses are looking for a more reliable banking partner who can provide innovative financing management tools, better customer experiences, and tailored financial products. Nonetheless, it is getting harder to differentiate one neobank from another regarding their focus and message because offering business banking accounts is getting commoditized.

Segmentation, international coverage and have their own banking licenses are ways to differentiate themselves used mainly by small fintechs. ⁶ The big ones add new products and services to make possible the monetization of their customer base. It’s pretty interesting how the binomial “segmentation x expansion” has affected the dynamic of making money.

Penta Case

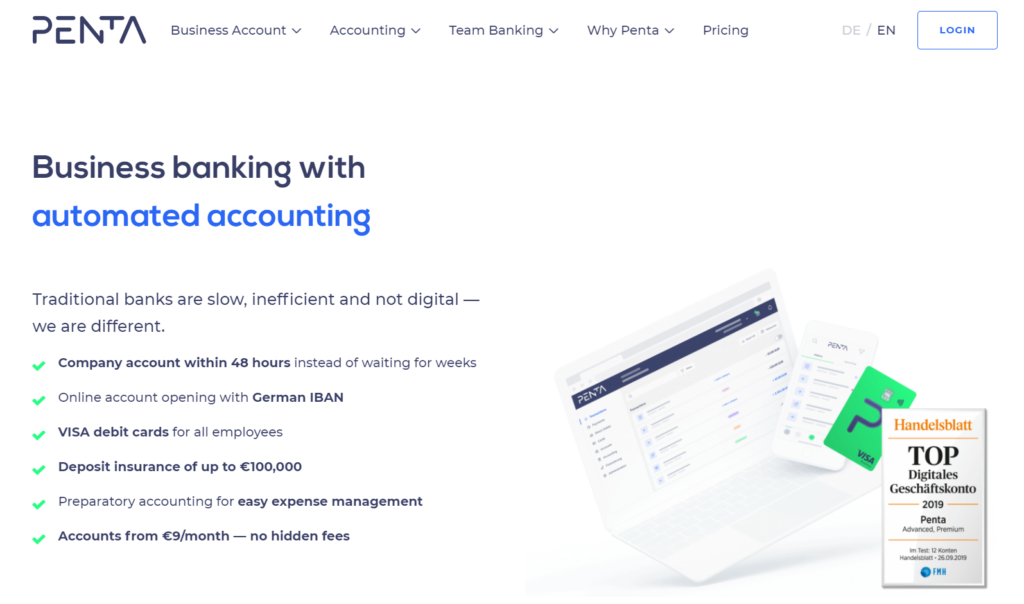

Known as the “N26 for corporate customers”, Penta is a young startup based in Berlin that offers a business-tailored account to smaller companies, sole proprietorships, freelancers and startups. It does not have its own banking license, which is why it works with Solarisbank.

Founded in December 2017 by Jessica Holzbach, Luka Ivicevic, Lav Odorovic, Aleksandar Orlic and Sir Gabriel Holbach, the neobank had raised EUR 47 million from business angels and venture capital firms like Inception Venture Capital, HV Capital and Finleap.

With the slogan “built by business owners for business owners”, the fintech reached 30,000 user accounts and a valuation of EUR 45 million in 2021. ⁷ By the end of the year, a clear goal of doubling this customer base was confirmed by Markus Pertlwieser, Penta’s CEO. He believes that Germany has a vast digital undersupply of four million potential customers. The business segment is highly attractive where the classic banks have been less on the move in recent years and not so much has been founded. ⁸

Furthermore, in order to differentiate itself from alternative providers, Penta makes possible the company budget management, allowing the leaders to give their employees and departments budgets to manage them independently.

The account also contains tools that integrate existing booking systems and work platforms such as Dropbox or Debitoor into the account management. In addition, customers can use the tools to make international transfers, make forecasts for their companies’ liquidity, and even get involved as developers to customize their account requirements.

Since the beginning, the customer focus is one of the reasons for Penta’s success. Its community is solid and accessible by Slack. There, customers determine which products and functions the neobank develops next and stay aware of updates, news, events, etc.

N26 Case

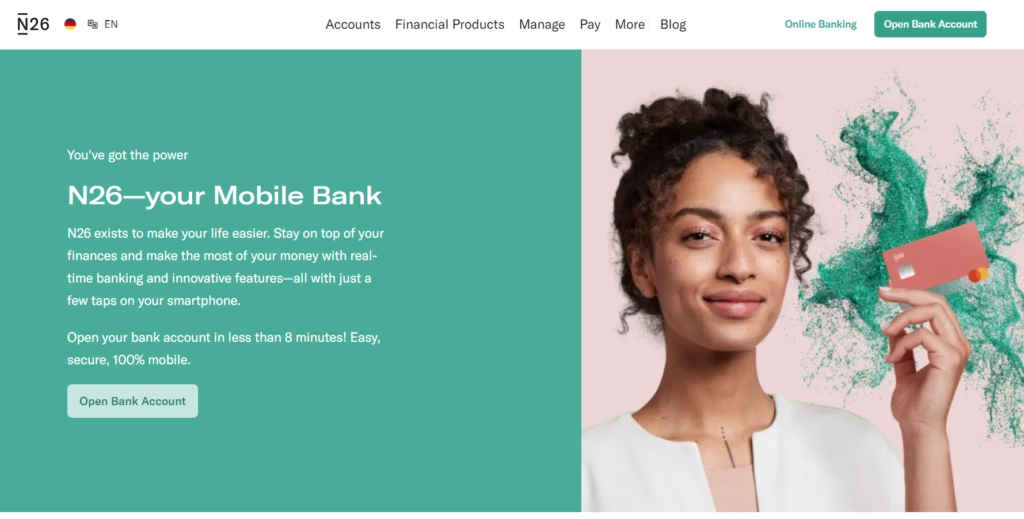

Founded in 2013 by Valentin Stalf and Maximilian Tayenthal, N26 is a German direct bank based in Berlin specialized in account management via smartphone. With more than 7 million customers reached in January 2021, the neobank currently offers its services in 25 countries, including Brazil.

Raised EUR 744 million since its beginning, N26 has a valuation of EUR 3.5 billion (February 2021) ⁹ and was voted number 1 in the 2021 Forbes list of the world’s best banks. It won awards in five countries, and placed as the top-ranked bank in Austria and Italy, ranked #2 in France, #4 in Spain, and #13 in its home market of Germany. ¹⁰ This rank is quite interesting and shows us a bit of the German financial market dynamic, very conservative and traditional in some segments.

However, this strong profile didn’t prevent the fintech from losing money in its global operation, reaching the amount of EUR 217 million in 2019 despite having doubled its revenues from EUR 43 million to EUR 100 million in the same period. ¹¹

A big driver of N26’s revenues has been its premium subscription-based accounts, for which it charges between EUR 4.90 to EUR 16.90 for a range of additional features. But Valentin believes that the big thing they are doing in Q1 and Q2 is focused on the marketplace, trying to integrate the entire experience.

Products such as trading and credit were included in the N26 app while the company takes fees from third-party providers. ¹² A great example of this dynamic is the neobank entrance in the insurtech space. The product “N26 Insurance” provides private liability insurance, home insurance, life insurance, pet insurance, and coverage for bikes, electronics, and other large purchases. Clients can take them, manage the scope and make claims through N26’s app. It can be bought as a standalone product or accessed as part of N26 Metal, the highest-price subscription plan. ¹³ ¹⁴

Despite the pandemic, the neobank said the number of business customers using their service has almost trebled in the past two years. The partnership between N26 and SumUp provides digital tools to allow freelancers, self-employed and entrepreneurs to accept cashless payments, helping their businesses thrive in today’s increasingly digitized world. ¹⁵

Nubank Case – the Brazilian market

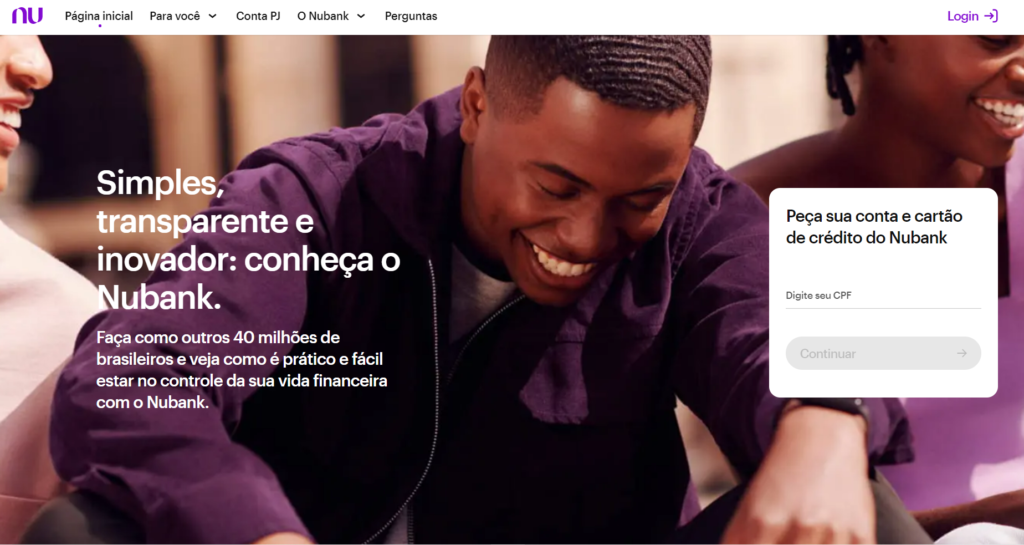

Nubank, the world’s most valuable privately-held bank based in São Paulo, was founded in 2013 by David Vélez, Cristiana Junqueira and Edward Wibel. The neobank opened space for the Brazilian banking transformation, breaking the hegemony between the five traditional banks that controlled 80% of the Brazilian market. These incumbents earn massive profits by lending at high-interest rates and charging exorbitant fees while providing lousy customer service. ¹⁶

With more than 40 million customers, the neobank currently offers its services in Brazil, Mexico and Argentina, and its first international office was opened at the end of 2017 in Berlin. The European team’s focus is on infrastructure and data engineering, but the mission is the same: to create products that reduce complexity and give its customers back control over their financial lives. ¹⁷

In June 2021, Nubank raised $750 million from Berkshire Hathaway Corporation, reached $30 billion value, becoming one of the most valuable startups in the world. The fintech leader increases its customer base by more than 1 million customers a month, which will make it the market leader in 2023 when it will complete ten years of life, beating the current leader, Banco do Brasil, with 200 years old. ¹⁸

The Brazilian fintech, ranked as the best Brazilian bank for three consecutive years by Forbes ¹⁰, is also expanding itself to other markets beyond payments and credit. It added investments in its portfolio through the Easynvest acquisition, which includes two own investments funds ¹⁹, and insurance offers through a partnership with Chubb. ²⁰

In July 2021, the neobank rolled out the “Nubank Ultravioleta”, a paid premium credit card with exclusive benefits such as cashback, VIP airport lounge access, travel medical insurance, and others. By launching a premium account tier that charges a monthly fee, Nubank is positioning itself to convert its huge client base into a steady revenue stream independent of the card usage. If it can convince just one out of every ten customers to become an Ultravioleta client, Nubank would stand to gain as much as EUR 31 million in revenue. ²¹

The business account, focused on individual and self-employed entrepreneurs, already supported 700 thousand customers. For this audience, which felt firsthand the importance of going digital in recent years, especially during the pandemic, the most significant advantage of being a fintech customer is the ease of receiving payments from its customers.

Do you want to know more about fintechs and the entrepreneurial ecosystem? Find out about my research in Germany HERE, and don’t miss the next chapters of this series on the German and Brazilian markets.

Read the first chapter of this series HERE.

Fonts

¹ Deutsche Bundesbank (2017). Financial Stability Review. November 2017. Frankfurt a.M.: https://www.bundesbank.de/resource/blob/667536/e3a7d39d28495bbc202ab94817314e7d/mL/2017-finanzstabilitaetsbericht-data.pdf

² Philippon, T (2019). On Fintech and Financial Inclusion. Mimeo. New York: https://www.nber.org/system/files/working_papers/w26330/w26330.pdf

³ Lumpur, K; Buch, C (2019). Digitalization, Competition, and Financial Stability: https://www.bundesbank.de/en/press/speeches/digitalization-competition-and-financial-stability-799792

⁴ Lochy, J (2020). Neobanks should find their niche to improve their profitability: https://bankloch.blogspot.com/2020/12/neobanks-should-find-their-niche-to.html

⁵ Klee, A (2021). An analysis of Europe’s key SME fintechs: https://rossrepublic.com/an-analysis-of-europes-key-sme-fintechs/

⁶ Chong, T (2020). Unpacking Neobanks for SMEs — Chapter 1 | Introduction to the Global Landscape: https://medium.com/arivalbank/unpacking-neobanks-for-smes-chapter-1-introduction-to-the-global-landscape-d06e629b42b

⁷ Penta Profile at DealRoom.com: https://app.dealroom.co/companies/penta

⁸ FinanceFWD#86 mit Penta-CEO Markus Pertlwieser: https://financefwd.com/de/penta-ceo-pertlwieser-podcast/

⁹ N26 Profile at DealRoom.com: https://app.dealroom.co/companies/number26

¹⁰ Gara, A (2021). The World’s Best Banks 2021: Financiers To The Looming Economic Recovery: https://www.forbes.com/sites/antoinegara/2021/04/13/the-worlds-best-banks-2021-financiers-to-the-looming-economic-recovery/?sh=2a8869412e17

¹¹ Woodford, I (2021). N26 spent €27m on failed UK bid, contributing to heavy losses: https://sifted.eu/articles/n26-losses-bulge-with-uk-expense/

¹² Browne, R (2021). German mobile bank N26 is thinking of making its first acquisition: https://www.cnbc.com/2021/01/28/fintech-ma-digital-bank-n26-is-thinking-of-acquiring-a-competitor.html

¹³ Tattersall, M (2021). N26 makes European insurance push to lure in new paid users: https://www.businessinsider.com/neobank-n26-sets-sights-on-insurance-expansion-to-drive-profitability-2021-4

¹⁴ Siliconcanals.com. German challenger bank N26 enters insurtech space, launches N26 Insurance; Here’s all you need to know: https://siliconcanals.com/news/startups/fintech/n26-enters-insuretech-space/

¹⁵ Rte.ie. N26 partners with digital payments company SumUp: https://www.rte.ie/news/business/2021/0419/1210821-n26-partners-with-digital-payments-company-sumup/

¹⁶ Kauflin, J (2021). How David Vélez Built The World’s Most Valuable Digital Bank And Became A Billionaire: https://www.forbes.com/sites/jeffkauflin/2021/04/07/fintech-billionaire-david-velez-nubank-brazil-digital-bank/?sh=28321ed76b27

¹⁷ Nubank’s Blog. Como funciona o escritório do Nubank em Berlim: https://blog.nubank.com.br/escritorio-do-nubank-em-berlim-como-funciona/

¹⁸ Manzoni Jr, R (2021). Nubank, a “ameaça roxa”, pode superar Banco do Brasil em 2023, diz relatório da XP: https://neofeed.com.br/blog/home/nubank-a-ameaca-roxa-pode-superar-banco-do-brasil-em-2023-diz-relatorio-da-xp/

¹⁹ Nubank’s Blog. Nubank lança fundos de investimento Nu Ultravioleta a partir de R$ 100: https://blog.nubank.com.br/nubank-lanca-fundos-nu-ultravioleta/

²⁰ PR Newswire Site (2020). Chubb and Nubank Launch Fully Digital Life Insurance Offering in Brazil: https://www.prnewswire.com/news-releases/chubb-and-nubank-launch-fully-digital-life-insurance-offering-in-brazil-301182589.html

²¹ Nubank’s Blog. Nubank Ultravioleta: novo cartão vai reinventar a categoria premium: https://blog.nubank.com.br/nubank-ultravioleta-novo-cartao-vai-reinventar-a-categoria-premium/

0 comentário